Abstract

Because of various financial reasons, or a change in strategic focus, sometimes brands stop broad-reach media advertising for a year or longer. These long dark periods have not been subject to much study, so little is known about the likely consequences. This exploratory study addresses this omission by documenting the sales performance of 41 beer, cider, and spirit brands that advertised intermittently over almost two decades. Changes in aggregate brand sales are reported for the years when brands stopped advertising relative to the last advertised year. On average, brand sales declined immediately in the first year and every subsequent year of advertising cessation. Decline generally was faster for smaller brands and for brands that already were declining in sales before advertising cessation.

Management Slant

When brands stop broad-reach advertising for a year or longer, most likely, sales will decline and continue to decline year over year without advertising.

The average observed change in brand sales was –16 percent after one year without advertising, dropping to –25 percent after two years, and reaching –36 percent after three years.

Brand size and sales trajectory before advertising cessation affected the rate of sales decline; sales declined more rapidly for small brands and already declining brands.

Larger, growing brands often were observed to continue to grow after advertising stopped, but almost all smaller, growing brands immediately began to decline.

INTRODUCTION

A man who stops advertising to save money is like a man who stops the clock to save time.

(commonly attributed to Henry Ford)

Conventional wisdom assumes that the longer a brand goes dark (i.e., unadvertised), the more likely it is that sales will slip eventually into decline (Broadbent, 1989); yet companies frequently cut advertising budgets when they look to reduce costs or temporarily inflate profits. These budgets are an easy target, because advertising is one of a few large budget items that can be withdrawn at short notice and leave a business operating at a similar capacity.

Reducing advertising spend unlikely will result in an immediate decrease in sales or market share, which suggests that brands could save money on advertising periodically without suffering major consequences (Tellis, 2004). The long-term implications of these decisions to stop advertising, however, are not well documented or understood. This study investigates what happens to aggregate sales when brands stop spending on all broad-reach advertising media for 12 months or longer, with a comprehensive dataset from a single industry: alcoholic beverages, encompassing beer, cider, and spirits.

“Equity” Advertising is Different

It is important to note that this study is concerned with broad-reach mass-media advertising in what are considered to be rather image-driven product categories. The authors report on the effects of stopping what is commonly referred to as “equity,” “brand,” or “image” advertising; specifically, advertising on broad-reach media, predominantly television, which rarely mentions price, or product features. The brands are supported by other activities, such as price discounting, in-store promotions, and price-oriented advertising by retailers. These other efforts are expected to affect sales volumes immediately when they are turned on and off. They often are called “activations,” because they largely are focused on catching buyers who are about to make a category purchase. By contrast, equity advertising aims to reach all category buyers (and often goes beyond this), most of whom are light, infrequent category buyers who are expected to buy the brand even less frequently. This kind of advertising reaches many people who will not buy for many months. Any effect that such advertising has on sales therefore must be spread far out into time.

Two different theoretical views of how equity advertising works unsurprisingly lead to different predictions. The first theory sees advertising as primarily working to mold consumer beliefs and, hence, attitude toward the brand. This can happen by providing information, by influencing feelings, or (posttrial) by reinforcing or framing experience (Vakratsas and Ambler, 1999). This perspective includes postmodern views, such as advertising that constructs brands as myths, archetypes, or personalities. Under this theoretical perspective, “the contribution of advertising largely ceased when the brand’s image was created” (Broadbent, 1989, p. 23); apart from occasionally targeting advertising to young, new-to-the-category buyers, it is only really needed when the image of the brand needs to be repositioned or refreshed because of changes in consumer preferences. This view is supported by the enduring nature of consumer beliefs and brand attitudes (Solomon, 1992) and, hence, the stability of brand images over years.

An alternative theory is that equity advertising largely works through memory rather than attitude and that these memories are rather fragile and context specific. Under this view, the primary role of broad-reach advertising is to build and then maintain the brand’s mental availability, which is its propensity to be noticed or brought to mind in buying situations (Romaniuk and Sharp, 2002, 2004; Sharp, 2010). Even if it says nothing new, continuous advertising is, therefore, required to maintain the salience of the brand’s links to category purchase cues in the face of competitive memory interference (e.g., competitor advertising) and general forgetting. This view is supported by the low repeat rates for the brand beliefs of consumers when interviewed twice (Castleberry, Barnard, Barwise et al., 1994; Rungie, Laurent, Dall’Olmo Riley et al., 2005); by the contextual nature of attitudes (Foxall, 2002); by predictable differences in belief/image/attitude scores based on brand usage and, hence, brand size (Castleberry and Ehrenberg, 1990; Romaniuk, Bogomolova, and Dall’Olmo Riley, 2012); and by the low correlation between attitudes and behavior (Kraus, 1995).

Both theoretical perspectives predict some sales loss from broad-reach advertising cessation, but the attitude/image theory predicts less sales loss and certainly less immediately. In this theory, the primary source of lost sales is that the brand is failing to win its share of new buyers entering the category. It is important to note that the attitude/image theory suggests that activations and advertising targeted at new category buyers can substitute for broad-reach advertising. In contrast, the mental availability theory predicts more immediate sales decline from loss of mental availability across most buyers, especially the large number of light buyers, as well as from failing to win expected share among new category buyers.

Mental availability theory further suggests that smaller brands will suffer sales declines in particular. Smaller brands will suffer because they have lighter, less frequent buyers on average (and, therefore, fewer occasions to refresh brand memories via direct experience), and because of their lower mental availability among their buyers, activations will have less ability to compensate for zero advertising. The attitude/image theory is more ambivalent about brand size, as even small brands can enjoy a strong image (Keller, 1993) and so have the ability to shift their marketing support away from equity advertising toward targeted activations.

Some Empirical Evidence

Estimates of the rate of advertising decay vary across studies. Analyses using econometric models find almost all of the effect of advertising on sales typically occurs within three to nine months (Clarke, 1976; Hanssens, 1980; Köhler, Mantrala, Albers, and Kanuri, 2017; Leone, 1995). It is necessary to note, however, that this research stream typically refers to the decay in lifts due to an advertising pulse; that is, how quickly the sales spike decays, similar to campaign evaluations regularly conducted by brand managers, and to the evaluation of any after effects of a price promotion. Broad-reach or equity advertising, however, is not expected to result in sales spikes when it is turned on. It is largely expected to maintain sales; in other words, to maintain the brand on its current growth trajectory, preserve its market share, or stem decline in the face of new competition. Such maintenance advertising does not cause spikes because its sales effects are spread thinly over time and only can be observed in long periods of advertising cessation.

The mental availability theory predicts more immediate sales decline from loss of mental availability across most buyers, especially the large number of light buyers, as well as from failing to win expected share among new category buyers.

Studies that specifically examine advertising cessation (as opposed to proportionate reductions in advertising spend) are rare. Consequently, there is not very much available evidence to indicate how quickly sales decline would likely set in after advertising cessation and the possible rate of sales decline over longer periods of time.

There is a stream of research examining advertising and business cycles (reviewed recently by Dekimpe and Deleersnyder, 2018) where it is well documented that companies very often reduce advertising during a recession. A common finding is that cutting advertising generally leads to declining sales and profitability during and after the recessionary period. The studies, however, do not separate out reductions in spend from cessation of advertising, and given the unique conditions a recession presents, extrapolating these findings to times of economic stability is problematic.

Split-cable experiments provide alternative evidence linking changes in advertising spend to brand sales (e.g., Lodish, Abraham, Kalmenson, et al., 1995). Results from zero-weight tests specifically, which compare “no advertising” to “normal advertising weight” conditions, show that it is equally likely that sales will remain stable as decrease (Hu, Lodish, and Krieger, 2007; Hu, Lodish, Krieger, and Hayati, 2009; Lodish et al., 1995). In practical terms, if a brand decides to stop advertising for up to 12 months, there seems to be a 50/50 chance that this action will adversely affect sales or, alternatively, lead to cost savings without consequences. The apparent randomness of sales changes is interesting and prompts further questions: What factors help to explain why some brands lose sales when advertising is stopped and others do not? What happens to sales when brands stop advertising for more than 12 months?

The present literature lacks consistently documented cases of brands stopping advertising for long periods. Gathering many in-market observations of what has happened to sales when mass-reach advertising is removed from the marketing mix will shed light on the long-term outcomes for brand performance, what happens more or less often (and at what magnitude), and which important conditions will moderate outcomes.

The purpose of this study is to document what happens to sales across a large number of cases when brands stopped advertising. The method used in this study further demonstrates how common aggregated data can be used to address this gap in knowledge. The authors introduce a simple descriptive approach applied to over 20 years of data from the alcoholic beverage industry, which captures 57 instances of brands that stopped advertising for a year or longer. The method produces easily absorbed findings and is scalable for wider use. Regularities in sales patterns across these 57 cases and two conditions (brand size and previous sales trajectory) are described. Depicting marketing phenomena through descriptive research is an important step in advancing knowledge and providing support for marketing decisions (Ehrenberg, Barnard, and Sharp, 2000). Findings from this research will provide further evidence for the long-term effects of advertising investments.

BACKGROUND

Advertising Spending

Cessation of advertising is one part of a much larger advertising budgeting conversation, which revolves around how much a brand should spend on advertising and how best to manage or distribute that budget over time. Common questions include: Are we spending enough to defend our position? How much must we spend to grow the brand? Can we afford to not spend on advertising for a time? These are important questions for which there remain relatively few evidence-based answers or tools for determining the optimal advertising budget (Danenberg, Kennedy, Beal, and Sharp, 2016).

It is not altogether surprising, then, that judgment-based approaches to budget setting are the most popular among advertisers, of which the most common approach is to identify what is affordable (West, Ford, and Farris, 2014). Heuristic methods such as this, which have been criticized for being overly simplistic and unrelated to strategic marketing objectives, likely would result in the misallocation of resources. As long as judgment-based budget setting abounds, advertising dollars will remain largely defenseless against cuts by upper management (Danaher and Rust, 1994).

It is conceivable that some reduction in advertising spending is reasonable, at least in some conditions. It was suggested decades ago that many brands are overspending on advertising. One study summarized 11 tests involving reduced advertising weight over one or two years (Aaker and Carman, 1982). Of these 11 tests, 10 were associated with stable sales. Another study produced similar results from a series of in-market advertising experiments conducted at the Campbell’s Soup Company (Eastlack and Rao, 1989). They found that decreasing advertising weight had little effect on sales over a period of eight to 10 months. Tests that have looked at the reverse situation, in which advertising weight is increased, found that spending substantially more on advertising significantly increased sales only about half of the time (at the 80 percent significance level; Lodish et al., 1995). The logical conclusion is that advertising weight alone, adjusted up or down, often is not enough to substantively change aggregate brand sales in the short-to-medium term (up to 12 months).

Advertising weight alone, adjusted up or down, often is not enough to substantively change aggregate brand sales in the short-to-medium term (up to 12 months).

Determining benchmarks or “normal” levels of advertising spend gives some context for when these increases or reductions more or less likely would be effective. If a brand was overspending the amount that is needed to maintain its market position, for example, then reducing spend removes waste, and sales would not be expected to respond negatively. It is well documented that larger brands spend more on advertising than smaller brands (e.g., Binet and Field, 2007; Buck, 2001; Jones, 1990). Empirical observation indicates that it is not a simple linear relationship between market share and share of voice (SoV) but a curved-linear relationship. Larger brands tend to underspend on SoV relative to their market share, whereas smaller brands overspend on SoV relative to their market share to maintain their respective positions (Buck, 2001; Hansen and Bech Christensen, 2005; Jones, 1990).

Larger brands seemingly benefit from their substantive past investments to establish consumer brand preferences as well as advantages with respect to physical availability (e.g., distribution, price, product range). They rely on these historic factors to prop up present performance and increase the brand’s profitability. This very situation can also tempt financiers to “milk” large share brands by further underspending. Jones (1990) suggested that milking brands could imperil sales, and recent work has demonstrated that sales do decline when brands consistently underspend Jones’s advertising intensiveness benchmark over a five-year period (Danenberg et al., 2016).

It appears that brands can reduce advertising spend to gain efficiencies, but if they underspend the recommended benchmark for their size, then they are at risk of losing sales and market share. Sales losses may not occur in the short or medium term, but there is evidence for eventual decline over the long term, from which the brand may not recover. Notably, the aforementioned studies pertain to some level of advertising spend being changed to some other level of spend. Stopping advertising altogether should be considered extreme underspending and presents a unique case. The potential perils of reducing advertising spend, as indicated by these studies, may not, therefore, adequately represent the perils of not spending on advertising at all.

When Brands Go Dark

The earliest reported experiments on advertising cessation are from the 1960s. Anheuser-Busch tested the effects of different advertising weight levels on Budweiser beer sales and noticed that test regions that had been completely deprived of advertising showed no significant differences in sales from control regions (Ackoff and Emshoff, 1975). The advertising hiatus and associated sales stability continued for more than 18 months before slight declines appeared in monthly sales figures. After reinstating advertising spend levels equivalent to before the experiment, sales bounced back within six months. On the basis of these results, the researchers enacted several changes in advertising spending at Anheuser-Busch. From 1962 to 1968, cuts were introduced into more markets at deeper levels until the ad spend per barrel was less than half what it was at the start. During this period, both sales and market share increased. That study conceded that the changes in advertising spend could not be solely responsible for the organization’s growth over this time and that other (unspecified) company actions or market conditions also contributed. The study reinforced, however, that “the changes induced by the research described here [including advertising cessation] did not hurt Anheuser-Busch” (Ackoff and Emshoff, 1975, p. 12).

Split-cable tests captured by market research companies since the Anheuser-Busch experiments have provided larger datasets to examine what happens when brands go dark. The split-cable method identifies two matched samples of consumers (or markets) and delivers different amounts of advertising (traditionally, television) to each group. Aggregate sales are monitored across the samples over time, and differences observed are attributed to the advertising manipulation. Most split-cable tests have looked at different advertising spend levels (either up- or downweighting), but a subset of tests examined treatments with and without advertising, which are called zero-weight tests. In these tests, the control market maintains a “normal” level of advertising spend (i.e., unchanged from before the test period) while advertising is turned off in the treatment market. Across four studies (Hu et al., 2007; Hu et al., 2009; Lodish et al., 1995; Riskey, 1997), 158 zero-weight tests were reported, each lasting 12 months (See Table 1).

Zero-Weight Advertising Tests with Significant Changes in Sales Effects

Across studies, about half of the zero-weight tests show no change in sales when advertising stopped for 12 months. When a significant sales effect was observed, sales were lower in the dark market on average. It, again, appears that advertising cessation for prolonged periods does not always have an observable effect on sales, but if it does, there likely will be a decrease. Advertisers consequently should proceed with caution when considering a complete cessation of advertising and monitor closely for changes in sales over time (Tellis, 2004). The authors are mindful, however, that these studies cover a period of time when the carryover effects of past advertising are present (for about three to nine months, as previously discussed). If a brand stops advertising for more than 12 months, it is probable that sales declines will occur more often and be greater in magnitude. To the best of the authors’ knowledge, investigations of this nature have yet to reach the academic advertising literature. Thus:

RQ1: What happens to aggregate brand sales after a brand stops all mass-media advertising for a year or more?

It is likely that advertising cessation will affect different brands in different ways. Sales outcomes will vary on the basis of the different qualities of the brands themselves and/or the circumstances surrounding the advertising cessation. Two factors worthy of investigation are the size of a brand and its sales trajectory before advertising cessation.

Previous evidence strongly suggests that brand size should moderate advertising sales effects, which may extend to advertising cessation. Larger market share brands have greater market-based assets (Srivastava, Shervani, and Fahey, 1998; Sharp, 2010); they have wider physical availability (Wilbur and Farris, 2014), and years of previous advertising and brand usage have given them more mental availability among the population of category buyers (Romaniuk, 2016). Smaller brands are building such assets, so they should gain proportionately more from spending on advertising and lose more from cutting advertising. Split-cable weight tests report that the likelihood and magnitude of sales changes after a reduction in advertising weight are less for larger and established brands than smaller and new brands (Hu et al., 2009; Lodish et al., 1995; Riskey, 1997); so, larger brands appear more resistant to sales reacting (negatively) to a cessation in advertising, but for how long?

The sales trajectory of a brand is another important contextual variable. Marketing managers likely would consider past brand performance when setting advertising budgets, particularly when allocating across a portfolio (Low and Mohr, 1999). Money generally is invested where greater returns are expected. Perhaps money may be taken more commonly from brands that are not growing (to support other growing or profitable stable brands), presenting a potential bias. It is unlikely that brands already in steep decline before advertising cessation will stabilize or reverse trend because all advertising support has been retracted. Therefore, are declining brands that are denied advertising support destined to die and die quickly?

Extending Research Question 1, two conditions that may help explain how sales respond to advertising cessation are explored:

RQ2: How do brand size and previous sales trajectory affect aggregate sales trends after a brand stops all massmedia advertising for a year or more?

METHOD

Data

A global manufacturer of alcoholic beverages provided the data for this study. The dataset included two decades of advertising media spend and brand sales volume information spanning beer, cider, wine, spirits, premixed ready-to-drink (RTD) beverages, and nonalcoholic or “mixer” brands in the Australian market. This type of “as-it-lies” data collected from the normal operation of competitive brands presents something of a natural experiment, making it possible to document what happened to numerous brands that stopped advertising. Such an approach also has been used when category advertising is stopped (e.g., Capps, Bessler, and Williams, 2016).

The advertising data included brand- and variant-level media-spend estimates reported annually for 20 years, from 1996 to 2015. Expenditure was reported in Australian dollars across 10 media platforms: metro and regional television, metro and regional press, magazines, radio, online, cinema, out of home, and direct mail. Estimates were the best data available, as the company typically purchased media in packages for multiple brands and could not always calculate exact investments for individual brands. Nonetheless, the estimates (based on spot data collected and valued by The Nielsen Company) were detailed suitably to determine when a brand was or was not advertising in any calendar year.

The sales data tracked manufacturer volume sales to distributors and retailers. Records comprised brand and variant level sales reported monthly for almost 23 years, from July 1993 to April 2016. The data were normalized to nine-liter case equivalents for all brands and included both bulk keg sales and retail packs. Sales data were aggregated from months to calendar years. Alcohol is a highly seasonal category in Australia, so this aggregation not only smoothed the seasonal variation in sales but also converted sales to the same yearly format as the media spend data. To calculate brand market shares, category sales data were provided by the company and also supplemented with additional data from the online statistics portal Euromonitor: Passport. Yearly category sales volume (in nine-liter case equivalents) was available for cider and RTD beverages from 1996 to 2016, for spirits from 1997 to 2016, and for beer and wine from 2001 to 2015.

Identifying Advertising Stops

To begin, it was necessary to develop a definition of a “stop” to determine whether and when any brand stopped advertising across the dataset. Under normal market conditions, it seems unlikely that any competitive brand ever stops all forms of advertising completely (depending on the chosen definition of advertising). For consumer-packaged goods (CPG), packaging can be considered point-of-purchase advertising, and brand websites as owned media tend to remain active regardless of paid media decisions. In this study, advertising cessation refers to a massive reduction in a brand’s mass-reach advertising. Because media spend information was reported annually, the authors considered a year without advertising as any year when a brand’s total spend was less than one percent of its average annual spend over the 20-year period. This definition captured years with zero advertising spend across all media as well as times when large brands that spent multiple millions of dollars on advertising per year spent only a few thousand dollars on low-reach media, such as outdoor, which is practically equivalent to ceasing communications across category consumers.

Each brand’s media data were coded as having either “some spend” or “no spend” (i.e., advertised or unadvertised) each year. Some brands advertised in every year and so were excluded from analysis. Some brands stopped only once in two decades, whereas others had bursts of spending with gaps in between. In total, 57 cases from 41 brands were identified in which these brands cut all mass advertising media spending for one year or longer. These cases came from a range of alcohol subcategories, but most were beer (43 beer, five cider, four spirits, three RTD, one wine, and one mixer).

In 34 of these 57 cases, the brand remained unadvertised in the following year too, constituting a two-year stop in advertising. The other 23 brands either restarted advertising, reached the final year of the dataset, or were delisted from the market. In this continuing fashion, there were fewer cases of brands staying unadvertised as the length of time increased (See Table 2).

Cases of Advertising Stops

Analyses

In all 57 cases, the sales volume of a brand in its last advertised year, immediately before stopping, was converted to a value of 100, and sales volumes in the following unadvertised year(s) were indexed relative to this value. This conversion reveals the proportional change in sales from that last advertised year after advertising cessation. An index changing from 100 in the “base year” to 80 in the (first) “no-advertising year,” represents, for example, a 20 percent decrease in sales after advertising cessation. The index measure is comparable across brands of different sizes and can be used to assess sales changes after one year without advertising, then two years, and so on, across cases. Once all cases were indexed, the average index in each year was calculated to determine the average change in sales across all cases after one year without advertising, then two years, and so on.

To establish the sales trajectory before advertising cessation, the authors looked at brand sales in the year immediately before the last advertised year (which is also an advertised year) and indexed these sales against the base year also. This approach reveals the year-to-year change in sales immediately before advertising cessation, which provides important context for sales trends observed after cessation. A previous year index of 115, for example, shows that the sales for a brand were 15 percent higher than for the base year indexed at 100, which indicates the brand was in decline leading up to advertising cessation.

Cases also were classified into subgroups as per the two conditions of brand size and sales trajectory. Brands with average yearly sales less than 250,000 units were considered small brands, those with average yearly sales between 250,000 and one million units were considered medium, and those with average yearly sales of more than one million units were considered large. Cases were classified as stable if the difference between previous and base year sales was less than ±10 percent index points. Cases with change greater than ±10 percent were labeled as growing or declining respectively. These cutoff values were chosen to split the sample into three roughly equal groups for each condition. Near-equal numbers of cases were classified as previously growing (n = 18), stable (n = 19), and declining (n = 20) brands. Most of those growing cases were small brands. There were more cessation cases from small brands (n = 23) than from medium (n = 17) or large (n = 17) brands. Notably, brands did not change their size classifications throughout the duration of the dataset: Small brands were not reclassified as medium, or medium as large when growing, nor the reverse when brands declined.

Beyond descriptive analysis, regression modeling was used to demonstrate congruent validity. This made it possible to include further data and control for the influence of category sales changes.

RESULTS

Sales Trends after Advertising Stops

The sales indices for all cases in each year are summarized (See Table 3). Central tendency and dispersion are reported through the mean sales index and the standard deviation from the mean. The mean sales index across all cases after one year without advertising is 84, showing that sales after one year without advertising were 16 percent lower on average than in the previous advertised year. The mean sales index falls further below the base year in each additional unadvertised year. On average, sales were 25 percent lower than in the base year after two years without advertising, and 58 percent lower after five years without advertising. The base year is indexed at 100 for all cases, giving a standard deviation of zero in that year. Sales indices varied considerably in other years, as reflected by the standard deviation. Among the one-year advertising stops, for example, indices ranged from 175 to 3 (i.e., +75 percent to –97 percent in sales growth or decline, respectively).

Mean Sales Index for All Cases

The authors also report the proportion of cases that declined in sales after cessation (See Table 3). Of all 57 cases, 53 percent (n = 30) reported a sales index of 90 or less after one year without advertising. That is, brands that stopped advertising for 12 months experienced substantive sales declines about half of the time, which is in line with findings across split-cable tests. This proportion increases to 62 percent of 34 cases without advertising after two years, and 71 percent of 17 cases without advertising after three years.

The authors have plotted the dispersion of cases around the mean (indicated by the solid line) at each incremental stop length, which shows a clear downward trend in sales across cases year over year when brands remain unadvertised (See Figure 1).

Indexed Sales (All Cases) of Brands Stopping Advertising

Note: This chart omits one value in the “prior” year that is greater than 200 (374).

All brands that stopped advertising for four years or more saw sales fall below the base year (index 100), and sales stayed below the base year while advertising cessation continued. This result is partly because almost every case in which a brand indexed higher in the first unadvertised year than in the base year remained unadvertised for less than four years (i.e., brands that initially grew when unadvertised typically went back on-air within a couple of years). Noting that of all 57 cases, only 14 percent (n = 8) reported growth (i.e., the sales index was 110 or more in the first unadvertised year) after stopping advertising for one year, when 32 percent (n = 18) of cases were growing before they stopped advertising.

Sales Trends by Conditions

Mean sales indices then were calculated for the different brand size and previous sales trajectory classifications. Each brand size group (large, medium, and small) and sales trajectory group (growing, stable, and declining) contained more than 10 cases of advertising stops of one and two years, but the samples are smaller for stops of three years or more (See the Appendix for sample sizes). Regardless of these small sample sizes, all observations are reported and qualitatively explored.

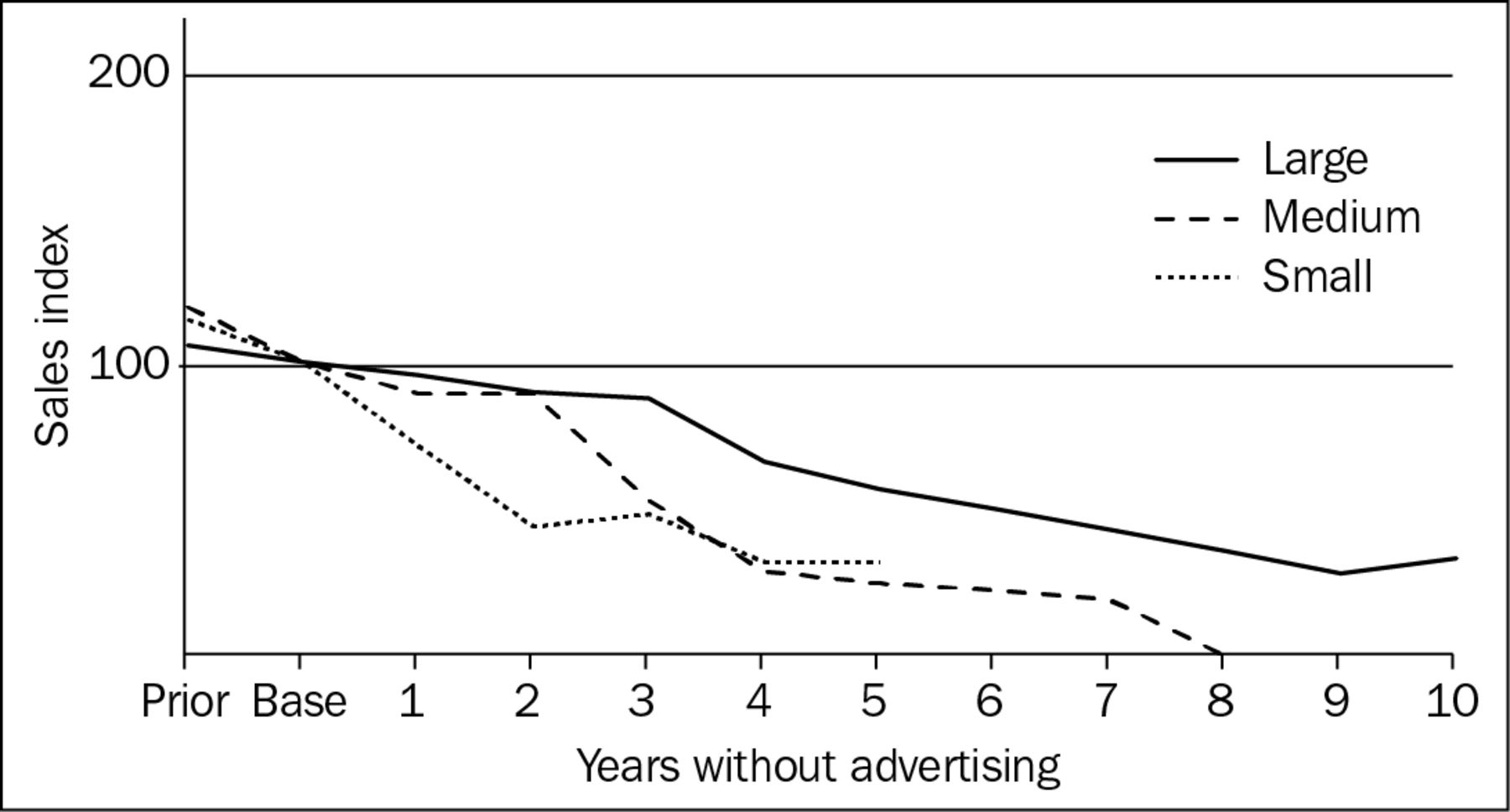

All brand size groups show declines over time, as indicated by their mean sales indices (See Figure 2). The most notable difference between size groups is that the average proportional decline over the long run was consistently less for large brands than for the medium and small brands. The slower average decline for large brands largely was expected, given previous research findings and also considering that relative proportional sales change will naturally appear less extreme from a larger base figure.

Mean Sales Index by Brand Size

Another notable difference between brand size groups is the length of time when brands stopped advertising. Some large brands went unadvertised for nine and 10 years (two cases for nine years and one case for 10 years). The longest case for medium brands was eight years, and no small brand went unadvertised for longer than five years. The steeper rate of decline for small brands likely increased the chance of being delisted sooner.

Average sales declines were much larger for brands already in sales decline before advertising cessation relative to previously growing and stable brands (See Figure 3). None of the previously declining cases (n = 20) captured in the dataset indexed above base year sales in any year after advertising cessation. One declining case eventually arrested its decline and even increased sales slightly (without resuming advertising) but did not return to its base year sales without advertising. Stable and growing brands stayed more stable, on average, for two years without advertising, with mean sales indices of 94 and 90, respectively.

Mean Sales Index by Previous Sales Trajectory

These averages were higher by virtue of the inclusion of cases that continued to grow after advertising cessation, even after two or three unadvertised years. For previously growing brands (n = 18), an almost equal number of cases indexed above and below 100 after a year without advertising (n = 10 versus n = 8, respectively). By comparison, a minority of cases indexed above 100 after a year without advertising for previously stable brands (n = 4 of 19), and none did so for previously declining brands.

Looking closer at previously growing brands only, an interesting finding emerges. All previously growing large and medium brands (n = 8) continued on an upward trend after advertising cessation, with sales indices greater than 100 in the first two unadvertised years. In all of these cases, advertising resumed after one or two years. Most previously growing small brands (n = 8 of 10 cases) dropped below 100 after one year without advertising, and all dropped below 100 after two years. These two groups of growing brands were similar in other respects: Each contained cases that were previously growing by similar magnitudes before advertising cessation, and all included brands from different alcohol subcategories, such as beer, cider, and spirits.

Regression Modeling

Multiple regression was used to quantify the relationships between brand size (average yearly sales log-transformed), previoius sales trajectory (percentage change in sales before advertising cessation), and change in sales after advertising cessation.

Category growth/decline also was included in the model. As noted earlier, category sales records for beer and wine only were available from 2001; hence, nine of the 57 cases in which a brand stopped advertising could not be matched with category-level data and so were omitted from the model. For the remaining 48 cases, category growth/decline was calculated as the year-to-year percentage change in category sales volume in the year(s) the brand stopped advertising. A Spearman’s rank correlation showed no significant relationship between brand sales changes and category sales changes, rs = .18, p = .21 (two-tailed). Despite lacking a clear relationship, the category growth/decline variable was still included in the multiple regression to explore its possible incremental benefit to the model.

The model is significant, with an R2 of .36, F(3, 44) = 8.2, p < .001. Both previous sales trajectory and brand size were significant predictors of brand sales changes after advertising cessation. Standardized beta weights show that previous sales trajectory (B = .50) more strongly predicts sales changes than brand size (B = .35). The model further suggests that the effect of category growth/decline on changes in brand sales after advertising cessation is relatively minor (B = –.04). The VIFs range from 1.002 to 1.041; hence, there is no concern regarding multicollinearity among the explanatory variables.

DISCUSSION

The sales of a brand are like the height at which an airplane flies. Advertising spend is like its engines: While the engines are running, everything is fine, but when the engines stop, the descent eventually starts.

(Broadbent, 1989, p. 23)

Advertising increasingly is being held accountable, and many marketers must present some case to retain their advertising budgets. It has proved challenging to build an evidence-based case for maintenance or “equity” advertising, because it is difficult to see the sales effects of this investment. The value of equity advertising is effectively demonstrated here by observing the consequences of its absence.

This study contributes to the literature through its novel approach to documenting the long-term effects of advertising budgeting decisions, specifically the decision to go dark on all broad-reach advertising media. Using descriptive analyses incorporating the advertising spend of many brands over two decades, this study shows the effects of advertising cessation for long periods on aggregate sales for beer, cider, and spirits brands. Multiple regression was used to check whether the conclusions from the descriptive analysis were consistent with statistical estimates, which they were. This work also identifies two key explanatory variables (brand size and previous sales trajectory) that affect sales responses when alcohol brands stop advertising, which should be incorporated in future research.

All previously growing large and medium brands continued on an upward trend after advertising cessation, with sales indices greater than 100 in the first two unadvertised years.

The authors observed that when broad-reach advertising media spend was stopped, most alcohol brands lost sales or suffered slower growth immediately in that first year of cessation. Decline became more common as brands went longer without advertising. Across brands of different sizes, and on different sales trajectories, relatively few avoided this fate.

Sales decline was more immediate and greater, on average, for small-share brands than for larger-share brands. Large and medium brands experienced some initial stability after stopping, on average, which is consistent with reports from split-cable studies (Hu et al., 2009; Lodish et al., 1995; Riskey, 1997). The findings, however, further indicate that, if left unadvertised for more than two years, large and medium brands also invariably slip into decline. For these brands, Broadbent’s plane analogy, quoted earlier, appears apt: Larger brands can cruise along for a time before descent starts. The plane analogy, however, implies accelerating decline, which was not observed. Across all cases, the average rate of sales decline year over year was rather moderate. The same was true for larger brands after the first two or three years without advertising. Although the data are messy (which is to be expected, given that these are real-world observations), and the number of cases dwindles as advertising cessation runs longer, alcohol brands do not commonly fall out of the market at an exponential rate when broad-reach advertising is turned off for multiple years. Still, the outcomes are generally detrimental for brands that go dark for such long periods.

Brands that were stable or growing before advertising cessation also experienced some initial stability. All previously declining brands, however, continued to decline after advertising cessation, regardless of their size.

One consistent exception to the broad declines documented across cases was for already-growing large and medium-sized brands, which all continued increasing in sales for two years after advertising cessation (and from there, were readvertised).

Forcing brands to take turns going dark for long periods could have a net negative effect on the total portfolio in the long run.

Of the two theoretical perspectives discussed earlier, it is the authors’ view that the results fit best with the mental availability theory of how advertising largely works. That, for most brands, negative changes in sales occur in the first year of cessation supports the idea that equity advertising which reaches even the lightest buyers of the brand is necessary for maintenance. There is enough variation in the individual cases, however, that it is possible that the attitude/image theory might still be apt under some conditions.

Managerial Implications

The finding that sales declined most commonly after brands stopped advertising offers some evidence—specifically for marketers of beer, cider, and spirits brands—to justify keeping their brands on-air each year. The authors acknowledge that this becomes a more complex decision when companies own multiple brands in the same product category (which is reasonably common in the alcohol industry, among others) and so must decide how to allocate scarce resources among a portfolio of brands. The authors do suggest, however, that a strategy of “this year we advertise these brands, and then next year, we advertise those brands” is probably ill advised. Forcing brands to take turns going dark for long periods could have a net negative effect on the total portfolio in the long run.

Removing advertising support for long periods from previously declining brands, perhaps to allocate those funds to other, “healthier,” brands in a portfolio, inevitably seems to prove fatal to those brands, regardless of their size. It is possible, even probable, that other forms of marketing support were removed along with advertising for these observed cases, which would have further assisted the demise of these brands. Even so, the cessation of advertising could have been premature, and the lifespan of these brands might have been longer if supported with broad-reach advertising. Knowing when to withdraw support in line with changing consumer trends (e.g., premium or low-calorie consumption) versus teasing out whether the brand team is just “losing faith” after a couple of poor performing advertising campaigns will remain a practical challenge.

Conversely, the authors observed that larger previously growing brands are relatively unaffected by advertising cessation and so can withstand an advertising hiatus for one or two years. This specific situation might represent an opportunity for companies to save money, improving profits. It is not certain, however, whether these brands would not have grown by more had they kept advertising.

Removing advertising support for long periods from small growing alcohol brands resulted in the most radical changes. For almost all of these cases, the sales trajectory immediately reversed from growing to declining. Small growing brands clearly need continued advertising support if they are to fulfil their growth potential. To increase sales and market share, these brands need to build mental availability across the market by exposing light, medium, and heavy category buyers to brand messaging, and broad-reach advertising helps to build and reinforce memories at scale.

The findings also provide support that brands should advertise with continuity over time, which proponents of mental availability theory recommend. Brand memories fade and must be refreshed and reinforced over time. Category purchases typically occur every week. Having extended dark periods means that there can be long gaps between consumers making a category purchase and their exposure to brand advertising. Even dark periods of several months can prove detrimental to supporting sales and market share (De Canha, Ewing, and Tamaddoni, 2020). In this gap, consumers may be nudged by advertising from a competitor or simply forget to think about the brand when it comes time to make a purchase, especially if they are a light category and/or brand buyer (Sharp, 2010). Therefore, rather than adopt a pulsing strategy, which would see brands turning equity advertising on and off periodically, a continuity strategy that reduces or excludes dark periods over the long term better supports brand performance (Gijsenberg and Nijs, 2019).

Limitations and Future Research

A key limitation of this study is the inability to control for other potential confounding variables. The analysis examined only mass-media advertising spend in relation to aggregate sales for the target brands; many other internal and external forces influence sales. Changes in pricing and promotions, distribution, competitor activities, and other marketplace forces likely contributed to the changes observed here. At a more macro-level, during the period of time studied, several disruptive changes also occurred in the Australian alcohol market, such as large company mergers and corporate takeovers, new competitor entrants, a notable trend toward premium craft brands, changes in physical and online distribution, changes in subcategory size and trends, and so forth. The authors acknowledge that the sole effect of advertising cessation on sales cannot be revealed without removing or controlling these other influences. Such controls were not possible in this study. The data come from the normal operation of real brands in a real market, and information on other variables was incomplete or absent. At the same time, it is quite remarkable that the results are as clear as they are without these controls.

Another limitation is that there is no transparency on how the dollars “saved” from the cessation of broad-reach advertising were spent. It is possible that brands did not go completely dark but redirected their budgets to communications that were not captured in the dataset, such as previously mentioned “activations” advertising, event marketing or sponsorship, or social media and influencer advertising post-2004. The data do capture online spend, which started from 2008 but it is limited to display advertising and was consistently dwarfed by investments in television advertising in particular. Despite these data limitations, the data were like for like across brands and time.

When classifying the sales trends of brands (as growing, stable, or declining), relying on merely two consecutive years of data may have inaccurately reflected the long-term sales trends of these brands. Aggregate yearly sales can fluctuate randomly within a longer term trend, so some brands may have been misclassified. A remedy would be to observe sales for longer than two years before advertising stops. This was not possible in every case, and the additional criteria would have meant fewer cases to analyze.

Finally, the generalizability of the findings is as yet unknown, because the results pertain to one industry (alcoholic beverages, predominantly beer) in one country (Australia). The observed sales changes in this study, however, are similar to what has been reported from zero-weight tests (e.g., Lodish et al., 1995; Riskey, 1997). In those studies, the average change in sales over 12 months without advertising was –15 percent and –23 percent, whereas the average change reported in this study is –16 percent for the same time period. The data from the previous studies came from a mix of product categories found in supermarkets (e.g., food, cleaning, and beauty products). The authors suspect that the findings of the current study and subsequent recommendations are not confined to beer, cider, and spirits brands and that the broad patterns and important conditions identified likely will generalize. Replication is encouraged to reveal the extent to which the direction and precise magnitude of patterns identified are common (or not) to other products and services and other market conditions (durable products, emerging markets, categories with varied levels of advertising intensity, etc.). Fortunately, the practical approach used here should be straightforward to extend to many industries.

ABOUT THE AUTHORS

Nicole Hartnett is a senior marketing scientist at the Ehrenberg-Bass Institute for Marketing Science, University of South Australia. She has a keen interest in advertising creativity and effectiveness, considering measurement approaches and managerial decision making. Her research in these areas has been published in the Journal of Advertising Research, Journal of Advertising, and European Journal of Marketing.

Adam Gelzinis is a customer insights business partner for Endeavour Group, Australia’s largest integrated drinks retail and hospitality business. He coauthored this paper as a master’s candidate at the Ehrenberg-Bass Institute.

Virginia Beal is a senior marketing scientist at the Ehrenberg-Bass Institute. Her research focuses on advertising effectiveness, media usage, and scheduling, and it has been published in the Journal of Advertising Research, Journal of Business Research, and International Journal of Advertising.

Rachel Kennedy is a research professor, director, and a cofounder of the Ehrenberg-Bass Institute. Her research is focused on advertising and media knowledge to help grow brands. Kennedy is on a number of journal editorial boards, and her work can be found in the Journal of Advertising Research, Journal of Advertising, Journal of Business Research, and Journal of Retailing and Consumer Services, among others.

Byron Sharp is a professor of marketing science at the University of South Australia and director of the Ehrenberg-Bass Institute. He serves on the editorial boards of six international journals. Sharp’s research on loyalty and brand performance has been published in more than 100 journal articles and conference papers, and he is the author of How Brands Grow (Oxford University Press, 2010), and Marketing: Theory, Evidence, Practice, second edition (Oxford University Press, 2018).

Appendix Cases of Advertising Stops Classified into Conditions

- Received February 3, 2020.

- Received (in revised form) May 18, 2020.

- Accepted July 13, 2020.

- Copyright © 2021 ARF. All rights reserved.

REFERENCES

Vol 64 Issue 3

{kind=link}

{kind=link}

{kind=link}